S&P 500

Dow Jones

Nasdaq

10-Year US Treasury Yield

British Pound per USD

Euro per USD

USD per Yen

Swiss franc per EUR

U.S. News

ISM Manufacturing PMI

- Manufacturing PMI surged to 55.6% in July — up 2.3 points from June and the highest reading since May 2022 — comfortably beating the roughly 54% consensus and marking the sector's seventh consecutive month of expansion.

- Production jumped 6.3 points to 58.5%, the strongest reading since November 2021, while the Employment Index returned to expansion for the first time in 33 months at 52.8%, with 60% of panelists reporting active hiring.

- Computer & Electronic Products emerged as the standout performer, with new orders, production, and employment all accelerating on the back of semiconductor and AI-driven demand, even as electronic components remained in short supply for a 17th consecutive month.

ISM Services PMI

- Services PMI ticked up to 54.1% in July from 54.0% in June — its 25th consecutive month of expansion — though the reading missed the 54.5% consensus and signaled a services sector that is resilient but losing some momentum.

- The Employment Index fell back into contraction at 47.4%, down 3.8 points and now below 50 for 12 of the past 18 months, diverging sharply from the strength seen in the manufacturing sector's hiring data.

- Prices Paid spiked 2.6 points to 70.3% — the fourth time above 70 in five months — as oil prices rose following the collapse of US-Iran talks, keeping inflation pressure firmly in focus ahead of Friday's jobs report.

Employment Report

- Nonfarm payrolls contracted by 23,000 in July — a stunning miss against the 83,000 consensus forecast and the first negative print in months — delivering a sharp shock to what had otherwise been a resilient economic narrative.

- The unemployment rate held at 4.1%, better than the 4.2% forecast, but average hourly earnings growth slowed markedly to 3.1% YoY versus 3.5% expected, suggesting wage pressure is cooling alongside softening labor demand.

- The miss follows a weak ADP print earlier in the week and a contracting ISM services employment component, reinforcing a consistent signal across multiple data sources that the labor market is decelerating faster than anticipated — sharply raising the odds of a September Fed rate cut.

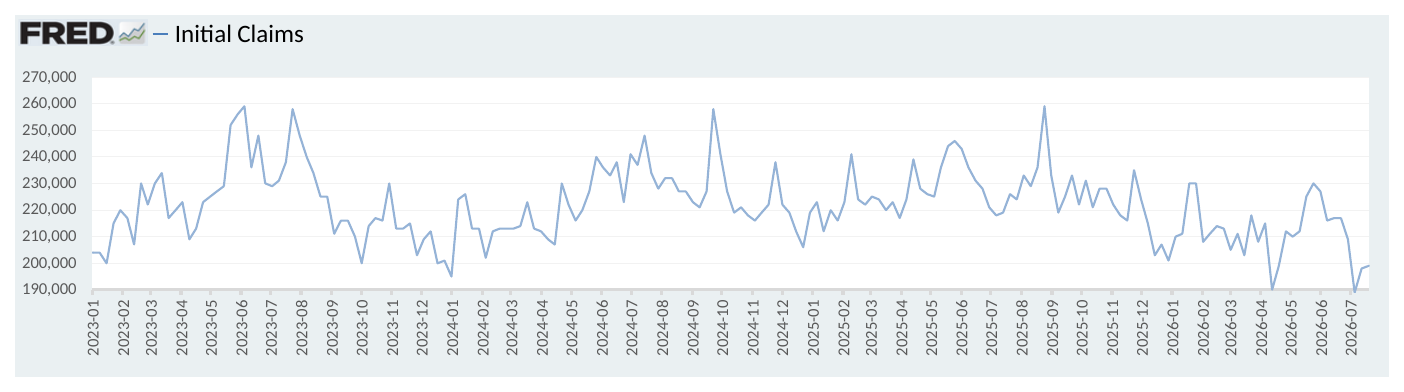

Jobless Claims

- Initial jobless claims, a measure of how many workers were laid off across the U.S., increased to 199,000 in the week ended July 31, up 1,000 from the prior week.

- The four-week moving average was 198,750, down 4,500 from the prior week.

- Continuing claims — those filed by workers unemployed for longer than a week — increased at 1.801 million in the week ended July 24. This figure is reported with a one-week lag.

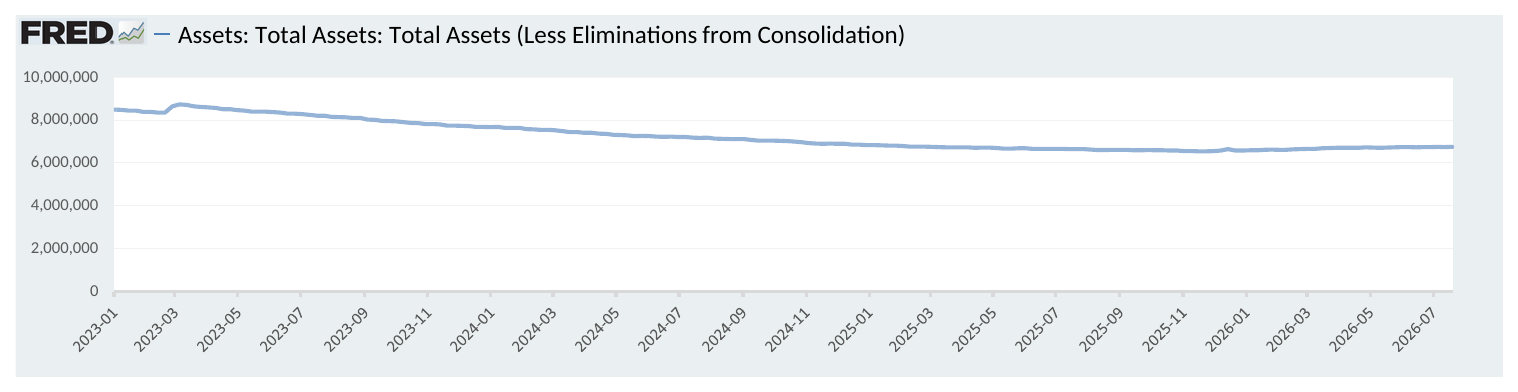

Fed's Balance Sheet

- The Federal Reserve's assets totaled $6.749 trillion in the week ended August 7, up $10.4 billion from the prior week.

- Treasury holdings totaled $4.525 trillion, up $5.5 billion from the prior week.

- Holdings of mortgage-backed securities (MBS) were $1.93 trillion in the week, down $16.0 billion from the prior week.

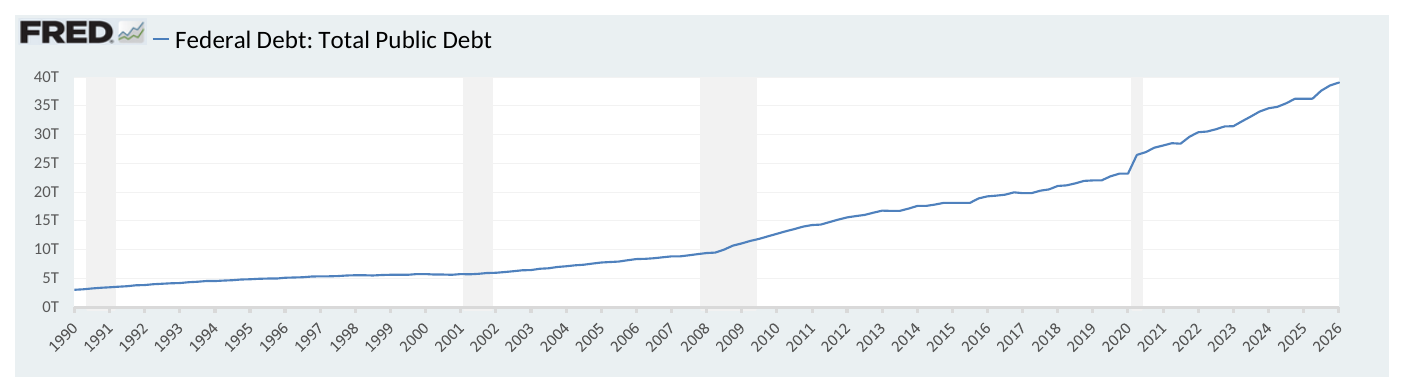

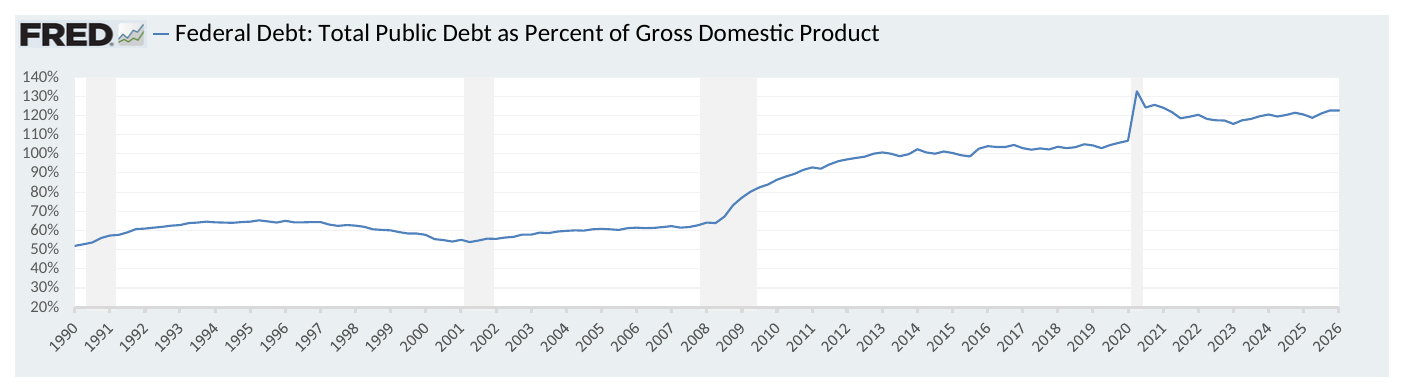

Total Public Debt

- Total public debt outstanding was $39.89 trillion as of August 7, an increase of 7.8% from the previous year.

- Debt held by the public was $32.15 trillion, and intragovernmental holdings were $7.73 trillion.

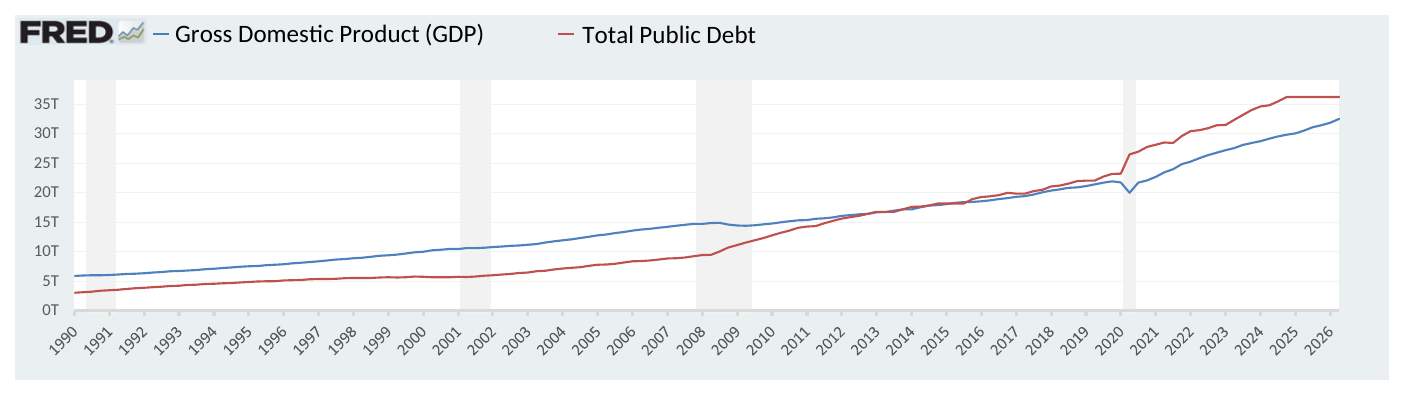

GDP

- The latest annualized U.S. GDP stands at $32.48 trillion as of June 30, 2026, an increase of 1.91% from the previous quarter, & an increase of 6.53% from the previous year.

- The total public debt-to-GDP ratio is at 121.52% as of June 30, an increase of 2.73% from the previous year.

Inflation Factors

CPI:

- The consumer-price index rose 3.5% in June year over year.

- On a monthly basis, the CPI decreased (0.4%) in June on a seasonally adjusted basis, after increasing 0.5% in May.

- The index for all items less food and energy (core CPI) fell 0.0% in June, after rising 0.2% in May.

- Core CPI increased 2.6% for the 12 months ending June.

Food & Beverages:

- The food at home index increased 2.7% in June from the same month a year earlier, and increased 0.2% in June month over month.

- The food away from home index increased 3.4% in June from the same month a year earlier, and increased 0.2% in June month over month.

Commodities:

- The energy commodities index decreased (9.5%) in June after increasing 6.7% in May.

- The energy commodities index rose 27.0% over the last 12 months.

- The energy services index rose 1.5% in June after increasing 0.7% in May.

- The energy services index rose 3.9% over the last 12 months.

- The gasoline index rose 26.7% over the last 12 months.

- The fuel oil index rose 42.9% over the last 12 months.

- The index for electricity rose 4.0% over the last 12 months.

- The index for natural gas rose 3.0% over the last 12 months.

Supply Chain:

- Drewry's composite World Container Index decreased to $4,254.73 per 40ft container for the week of July 31.

- Drewry's composite World Container Index has increased by 70.3% over the last 12 months.

Housing Market:

- The shelter index increased 0.1% in June after increasing 0.3% in May.

- The rent index increased 0.1% in June after increasing 0.3% in May.

- The index for lodging away from home decreased (2.5%) in June after increasing 2.6% in May.

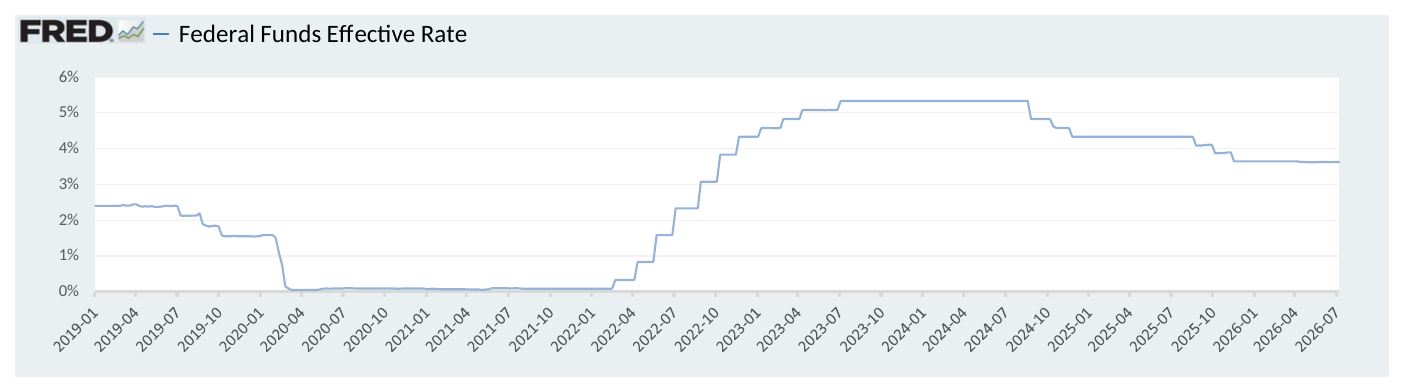

Federal Funds Rate

- The effective Federal Funds Rate is at 3.63%, down (0.01%) year to date.

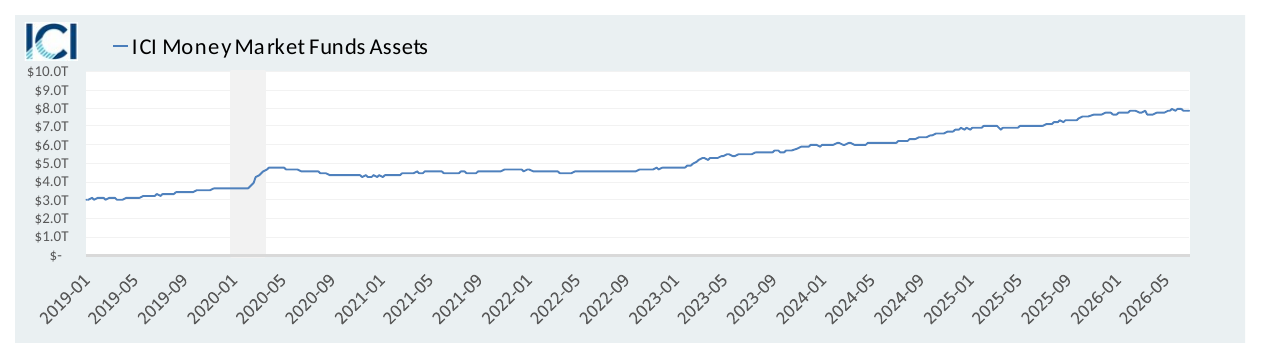

Money Market Funds

- Money market fund assets stood at $7.91 trillion as of August 5, 2026, up 0.7% from the previous week, & up 10.6% from the previous year.

World News

Middle East

- Oil futures whipsawed through the week on Strait of Hormuz reopening speculation, with WTI swinging from a 3.7% gain to $78.01 to a modest pullback to $76.85, as analysts cautioned that any diplomatic breakthrough would likely deliver only temporary market stability given Iran's enduring capacity to restrict the waterway again.

- Prices found renewed support from escalating regional instability, including a reported large-scale Houthi attack on Saudi-backed forces in Yemen and continued threats to Red Sea shipping — underscoring that even a Hormuz resolution would leave multiple other flashpoints capable of disrupting Middle East energy flows.

- Turkey, Saudi Arabia, and Pakistan signed a mutual defense pact in Mecca establishing a collective defense clause, under which an attack on any one signatory is treated as an attack on all three — a direct response to mounting uncertainty over the durability of the U.S. security umbrella following the Iran war.

- The agreement unites a nuclear-armed Pakistan, oil-rich Saudi Arabia, and NATO member Turkey in an unprecedented trilateral security arrangement, signaling that Gulf and regional powers are actively hedging against future Iranian aggression even as they remain structurally dependent on U.S. military support.

Europe

- German industrial production unexpectedly rose 0.2% in June, extending May's 0.7% gain and beating the flat consensus, with growth driven by strength in automotive, aircraft, and defense manufacturing even as energy costs climbed following the renewed Iran conflict.

- Factory orders jumped 3.1% and exports hit a record high in June, confirming net exports as the primary growth driver in a quarter that saw German GDP expand 0.2% — though economists caution the widening trade deficit with China, rising energy costs, and record-low Rhine water levels leave the recovery structurally fragile rather than durable.

- TotalEnergies agreed to sell a 50% stake in a 1.2 gigawatt European onshore solar and wind portfolio spanning Germany, Spain, France, and Poland to KKR in a deal valuing the assets at $2.08 billion including debt.

- In a separate transaction announced the same day, TotalEnergies agreed to acquire a 4 gigawatt renewables portfolio from Shell across Italy, the U.K., and Spain — signaling continued consolidation and active portfolio reshuffling among Europe's largest energy majors in the renewables space.

China

- China's exports surged 24% year-over-year in July — slightly below June's 27% but still topping economists' expectations — with semiconductor and computing equipment shipments tied to AI demand contributing more than 10 percentage points to overall export growth, the largest such contribution since at least 2002.

- Trade with the U.S. is reaccelerating despite recent retaliatory measures, with exports to America up 17% and imports up 15% year-over-year in July, as lower tariffs under the ongoing trade detente set the stage for an expected Trump-Xi meeting next month.

- Taiwan launched 10 days of military and civil defense exercises mobilizing 20,000 reserve troops, incorporating drone tactics drawn directly from Iran's asymmetric strategy against a more powerful adversary, as Beijing conducted its 20th joint combat readiness patrol of the year with 21 warplanes and nine warships around the island.

- The drills notably include a first-ever mobile internet slowdown near TSMC's Hsinchu hub and new decentralized command exercises designed to sustain resistance during a communications blackout — reflecting Taiwan's growing assumption that it may need to hold out against a Chinese invasion without immediate U.S. military support.

Japan

- The U.S. and Japan conducted a historic joint currency intervention on Friday to support the yen near 40-year lows, driven by slow Bank of Japan rate hikes and Iran war-fueled energy import costs on Japan's side and concern over Treasury market stability on the U.S. side, since Tokyo — the largest foreign holder of U.S. Treasurys — has committed to borrowing from the Fed rather than selling its bondholdings to fund any further defense of the currency.

Venezuela

- U.S.-backed talks between Venezuela's interim government and parts of the opposition began on August 1, aiming to establish a path toward democratic elections, but exclude prominent opposition leader María Corina Machado and lack a clear election timetable. The talks reflect the Trump administration's efforts to advance a political transition while supporting Venezuela's economic stabilization and reopening the country to U.S. investment.

India

- Indian companies are ramping up overseas acquisitions to diversify markets, access technology, and strengthen supply chains amid geopolitical uncertainty, with outbound investments reaching $14 billion in the first four months of fiscal 2026, compared with $18.7 billion in the prior full year. Major deals include Sun Pharma's $11.7 billion acquisition of US-based Organon and Persistent Systems' €1.3 billion bid for Germany-based Nagarro.

Colombia

- Far-right populist Abelardo de la Espriella — a criminal defense attorney who has represented paramilitary commanders and money launderers — captured 44% of the vote in Colombia's first-round presidential election, setting up a June 21 runoff against leftist Iván Cepeda that presents voters with the starkest ideological choice in the country's modern political history

Africa

- The WHO declared a global health emergency over an Ebola outbreak in Congo and Uganda, with around 80 deaths and over 200 suspected cases recorded — including cases in both countries' capitals — involving the rare Bundibugyo strain for which no approved vaccine or treatment currently exists

Cuba

- CIA Director Ratcliffe made a rare visit to Havana to warn Cuban officials they have a limited window to engage with the Trump administration, as the island faces severe fuel shortages, widespread blackouts, and growing street protests

Australia

- Australia is permanently diversifying its oil imports beyond Middle East suppliers and accelerating its renewable energy transition, even as it secures emergency fuel reserves to buffer against the ongoing Strait of Hormuz disruption

Canada

- Canada approved Enbridge's ~$3 billion Westcoast pipeline expansion, adding 300 million cubic feet per day of capacity as part of PM Carney's push to reduce U.S. trade dependence and boost Asian energy exports

Italy

- Trump publicly broke with Italian PM Giorgia Meloni — once his closest European ally — after she refused to send forces to the Strait of Hormuz and called his attacks on Pope Leo "unacceptable," leaving her isolated on both sides of the Atlantic

Commodities News

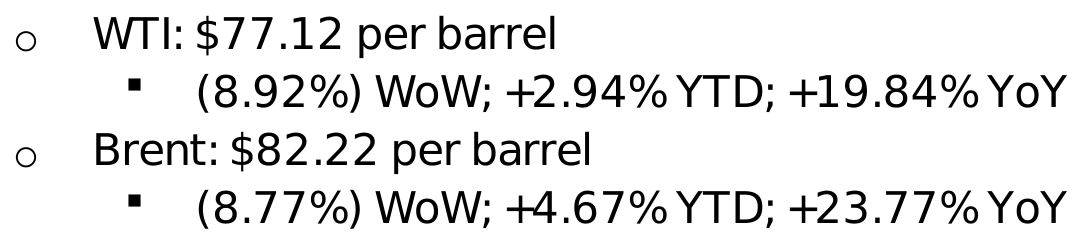

Oil Prices

- WTI: $77.12 per barrel

- (8.92%) WoW; +2.94% YTD; +19.84% YoY

- Brent: $82.22 per barrel

- (8.77%) WoW; +4.67% YTD; +23.77% YoY

US Production

- U.S. oil production amounted to 13.8 million bpd for the week ended July 31, up 0.0 million bpd from the prior week.

Rig Count

- The total number of oil rigs amounted to 588, flat from last week.

Inventories

Crude Oil

- Total U.S. crude oil inventories now amount to 407.0 million barrels, down (3.9%) YoY.

- Refiners operated at a capacity utilization rate of 96.5% for the week, down from 97.2% in the prior week.

- U.S. crude oil imports now amount to 5.683 million barrels per day, down 4.0% YoY.

Gasoline

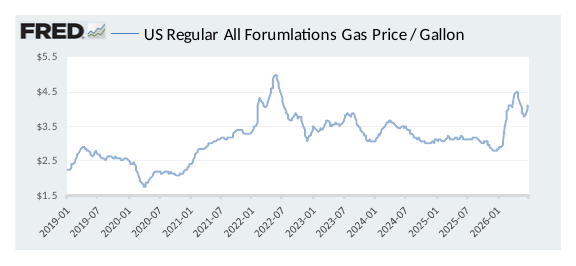

- Retail average regular gasoline prices amounted to $4.04 per gallon in the week of August 7, up 28.1% YoY.

- Gasoline prices on the East Coast amounted to $4.06, up 29.8% YoY.

- Gasoline prices in the Midwest amounted to $4.02, up 28.4% YoY.

- Gasoline prices on the Gulf Coast amounted to $3.71, up 30.9% YoY.

- Gasoline prices in the Rocky Mountain region amounted to $4.28, up 31.3% YoY.

- Gasoline prices on the West Coast amounted to $5.26, up 26.6% YoY.

- Motor gasoline inventories were down by 1.6 million barrels from the prior week.

- Motor gasoline inventories amounted to 209.7 million barrels, down (7.7%) YoY.

- Production of motor gasoline averaged 9.57 million bpd, down (2.4%) YoY.

- Demand for motor gasoline amounted to 9.031 million bpd, down (0.1%) YoY.

Distillates

- Distillate inventories decreased by 3.5 million in the week of August 7.

- Total distillate inventories amounted to 107.2 million barrels, down (5.1%) YoY.

- Distillate production averaged 5.230 million bpd, up 2.4% YoY.

- Demand for distillates averaged 3.941 million bpd in the week, up 5.9% YoY.

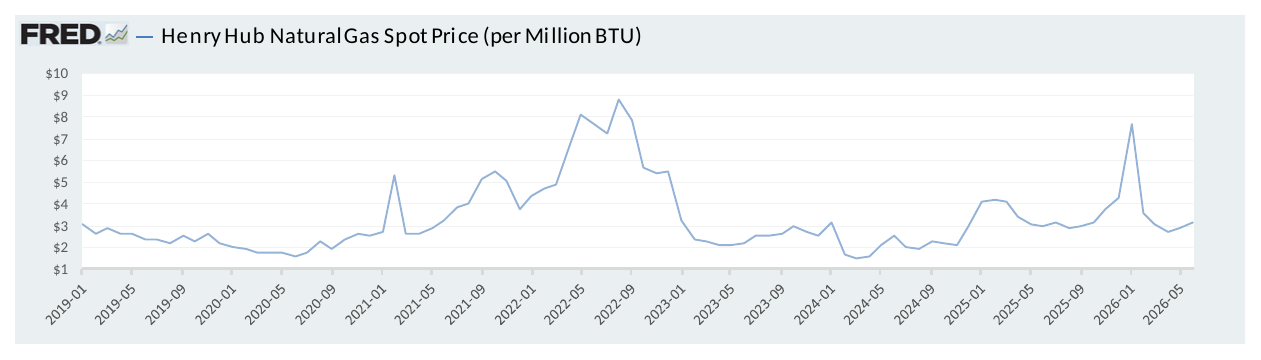

Natural Gas

- Natural gas inventories increased by 33 billion cubic feet last week.

- Total natural gas inventories now amount to 3,117 billion cubic feet, down (0.4%) YoY.

Credit News

High-yield:

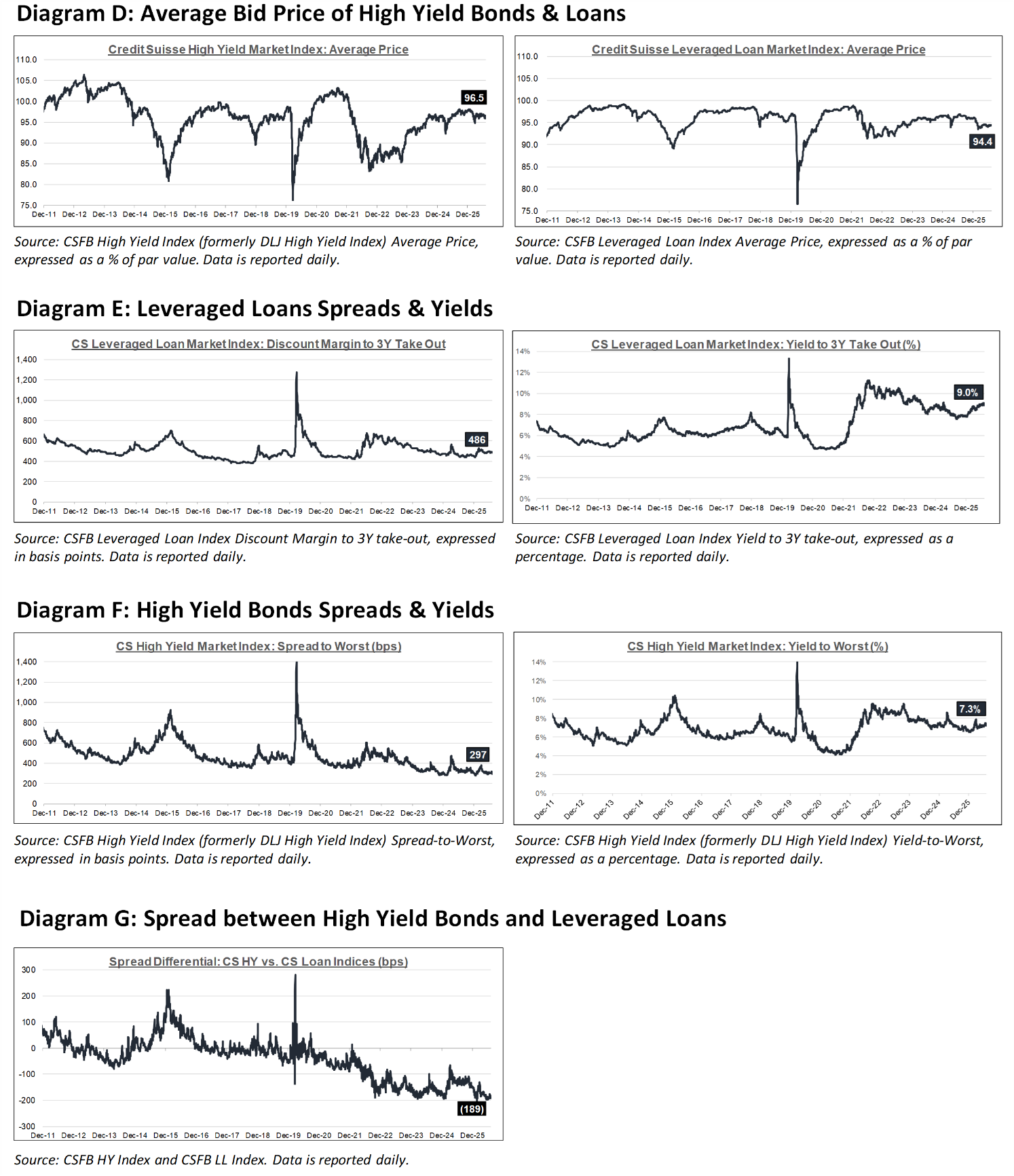

High yield bond yields decreased 17bps to 7.26% and spread tightened 16bps to 297bps. Leveraged loan yields decreased 4bps to 8.97% and spread tightened 7bps to 486bps. WTD high yield bond returns were positive 55bps and WTD leveraged loan returns were positive 25bps. 10yr treasury yields decreased 9bps to 4.65%. The rally was supported by a strong HY earnings season, reduced odds of a September Fed rate hike and strong technical with $2bn inflow amid $3.3bn of issuance. From a sector stance, cable/sat. (+0.76% w/w) and technology (+0.61%) outperformed the index, whereas telecom (-0.18%) and retail (-0.16%) underperformed.

Week ended 08/07/2026

Yields & Spreads¹

Pricing & Returns¹

Fund Flows²

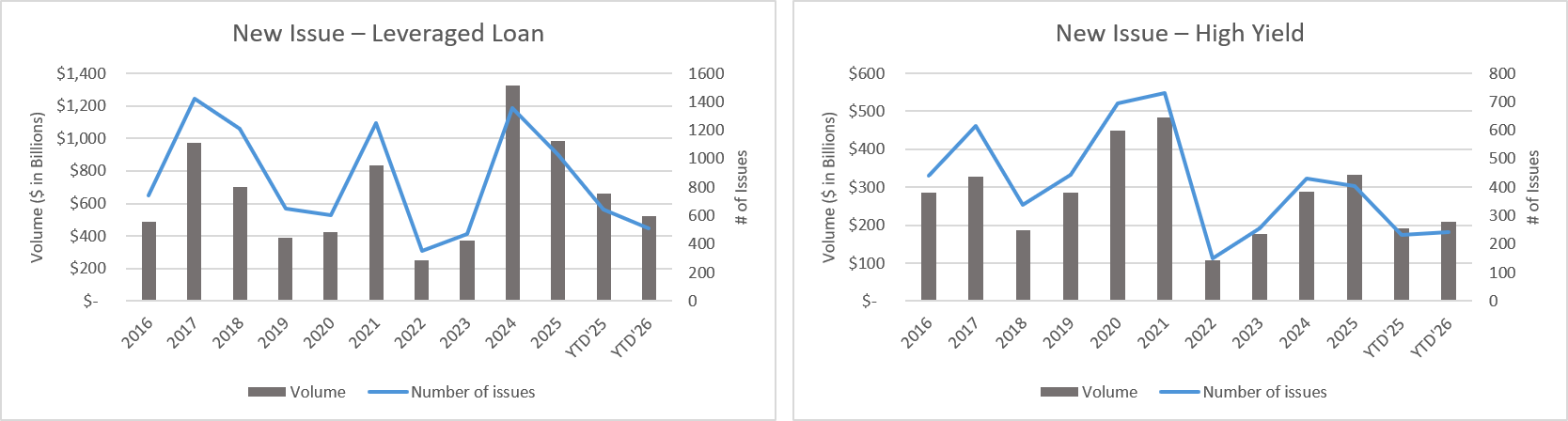

New Issue²

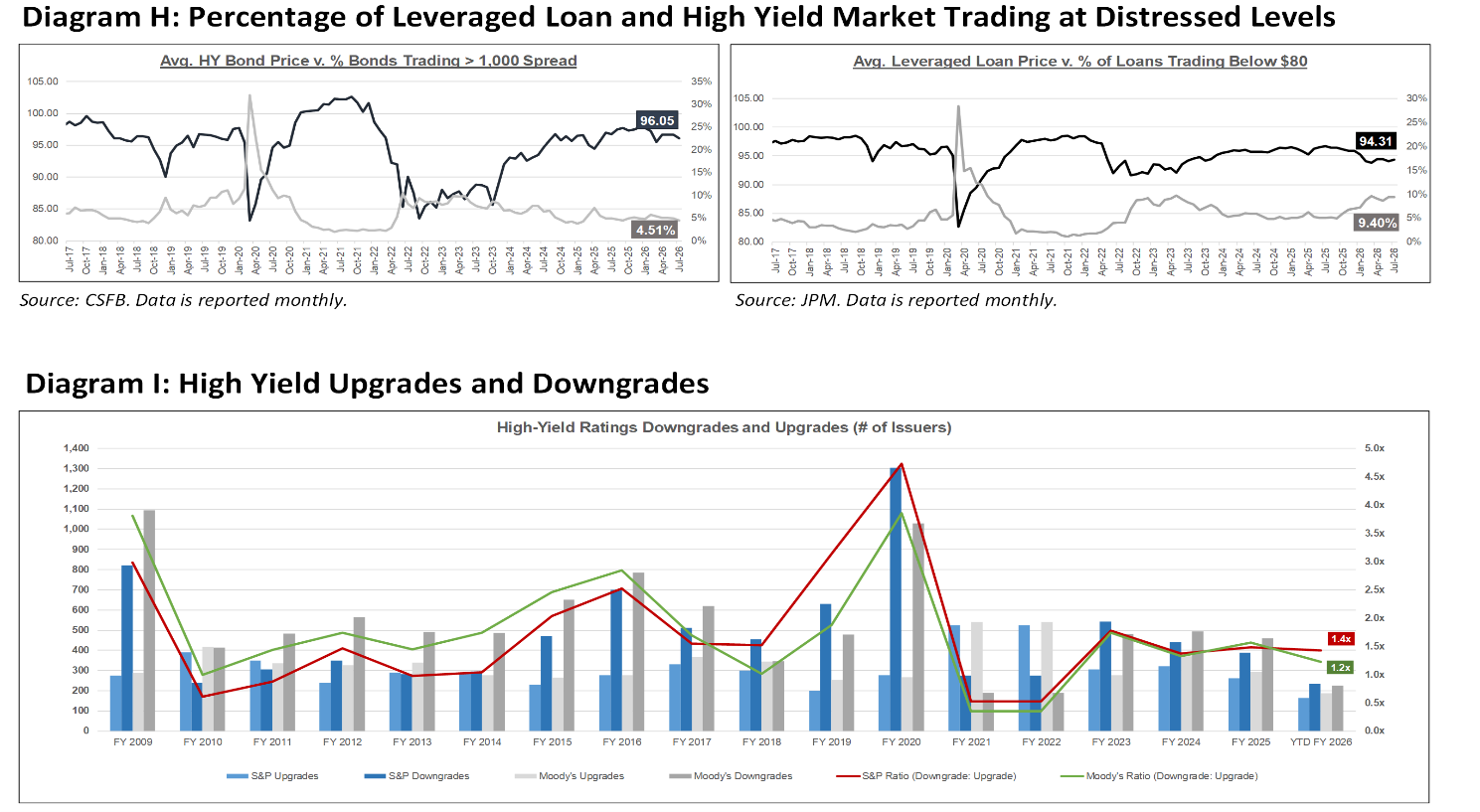

Distressed Level (trading in excess of 1,000 bps)²

Total HY Defaults

Leveraged loans:

Week ended 08/07/2026

Yields & Spreads¹

Pricing & Returns¹

Fund Flows²

New Issue²

Distressed Level (loan price below $80)¹

Total Leveraged Loan Defaults

Default activity:

- Most recent defaults include: Hughes Satellite Systems ($1.5bn, 8/2/2026), Unifrax Investment ($3.1bn, 7/26/2026), Dish DBS ($9.8bn, 6/30/2026), QVC Group ($2.2bn, 4/16/2026), Cumulus Media ($641mn, 03/05/2026), Trinseo ($390mn, 02/17/2026), Beasley Broadcasting Group ($189mn, 02/01/2026), Nine Energy Service ($300mn, 02/01/2026), Multi-Color ($4.5bn, 01/29/2026), and Pretium Packaging ($201mn, 01/28/2026).

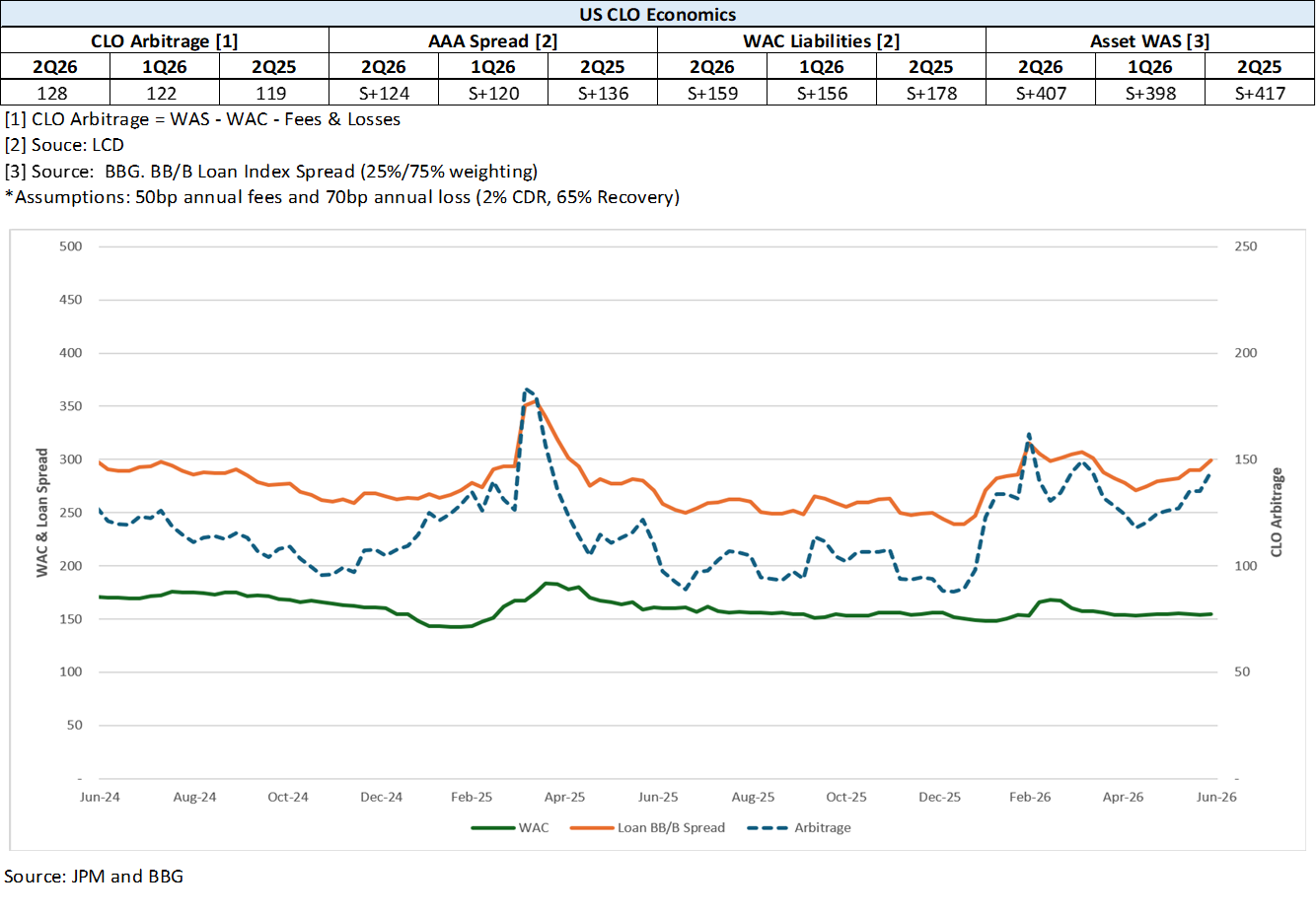

CLOs:

Week ended 08/07/2026

New U.S. CLO Issuance²

New U.S. CLO YTD Issuance²

Note: High-yield and leveraged loan yields and spreads are swap-adjusted

¹ Source: Credit Suisse High Yield and Leveraged Loan Index

² Source: JP Morgan

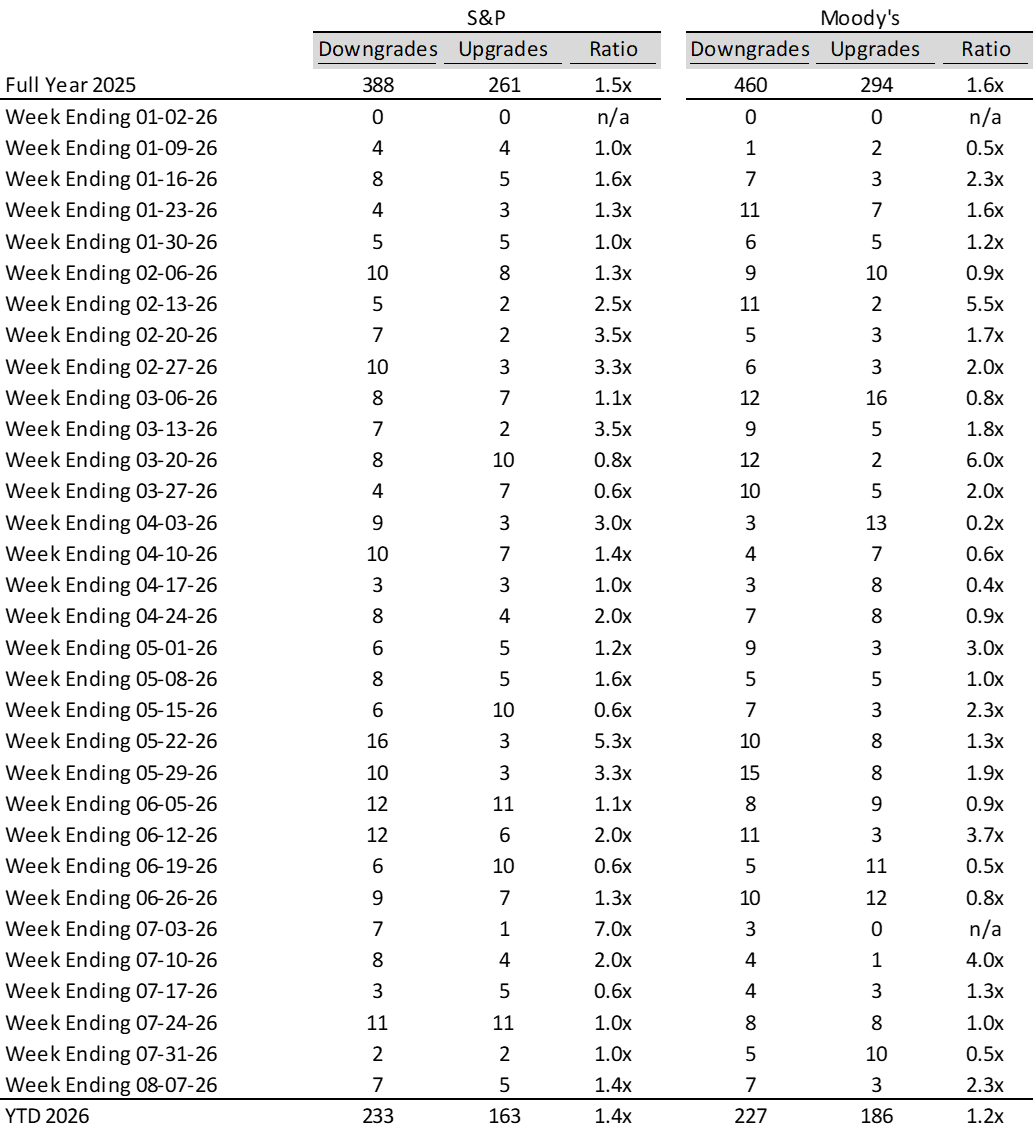

Ratings activity:

S&P and Moody's High Yield Ratings

Source: Bloomberg

Appendix:

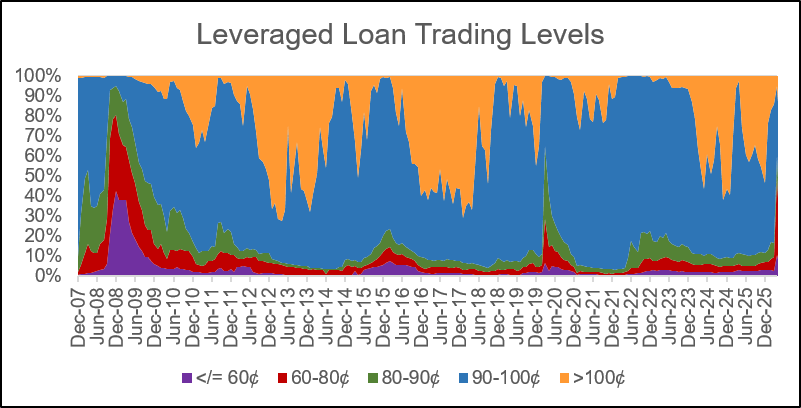

Diagram A: Leveraged Loan Trading Levels

Source: Credit Suisse Leveraged Loan Index

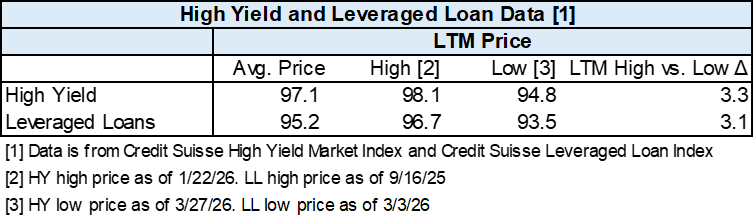

Diagram B: High Yield and Leveraged Loan LTM Price

Diagram C: Leveraged Loan and High Yield Returns

Diagram J: New Issue - Leveraged Loan and High Yield

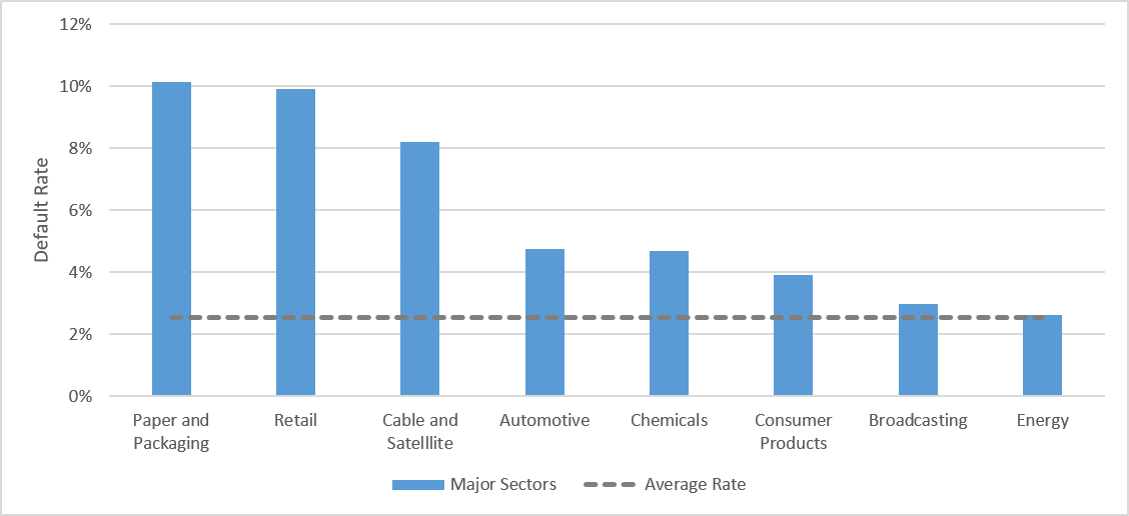

Diagram K: Leveraged Loan + HY Defaults by Sector – LTM

Source: JP Morgan Default Monitor

Diagram L: CLO Economics

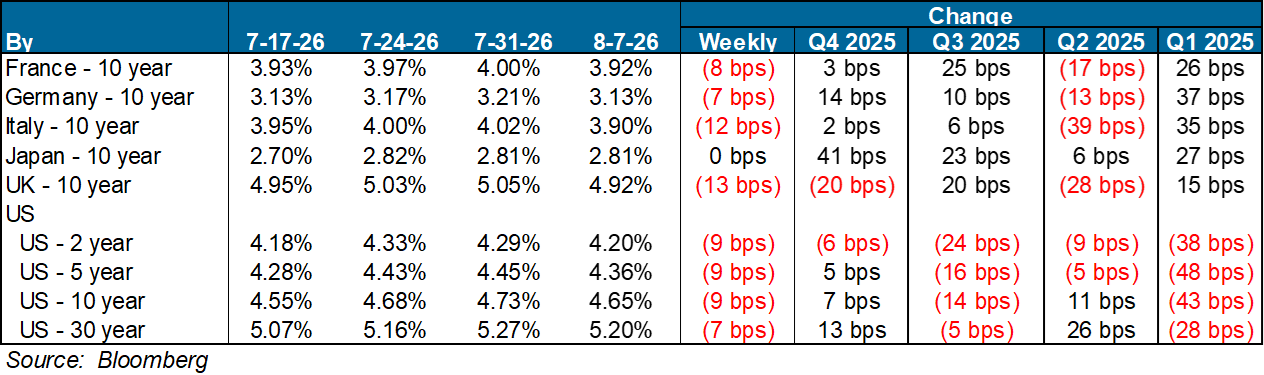

Diagram M: Developed Country Govt. Bond Yields (%)

Diagram N: S&P 500 Historical Multiples

Source: S&P Capital IQ

Diagram O: U.S. Middle-Market M&A Valuations (EV/EBITDA)

Source: Pitchbook

Diagram P: U.S. Large Cap M&A Valuations (EV/EBITDA)

Source: Pitchbook

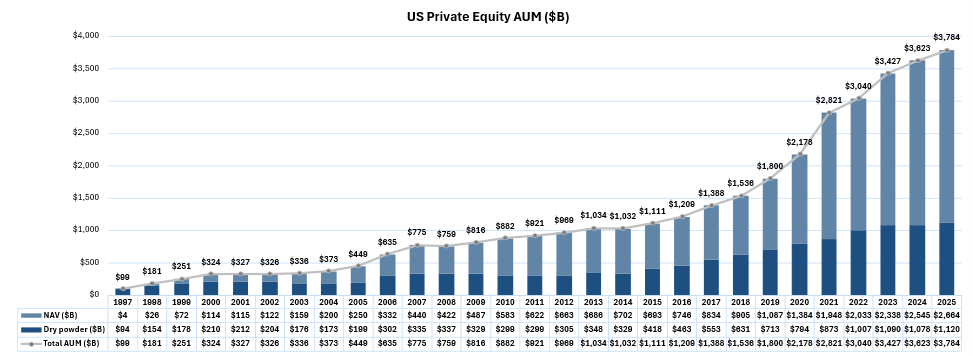

Diagram Q: Dry Powder for All Private Equity Buyouts ($B)

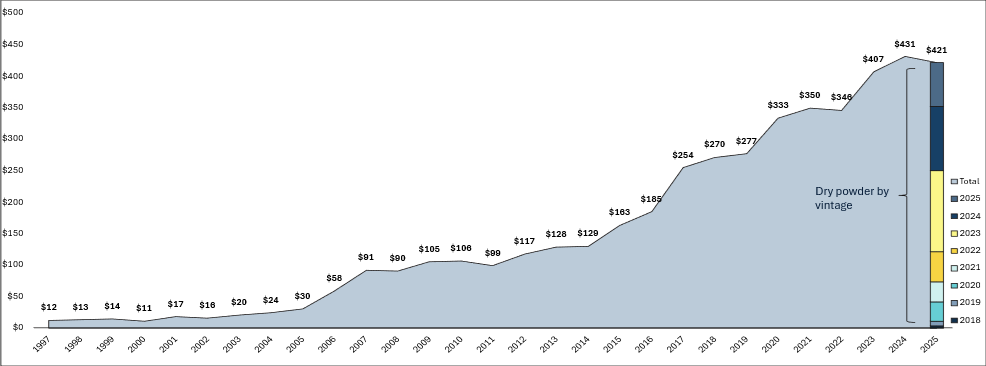

Diagram R: Dry Powder for All US Debt ($B)

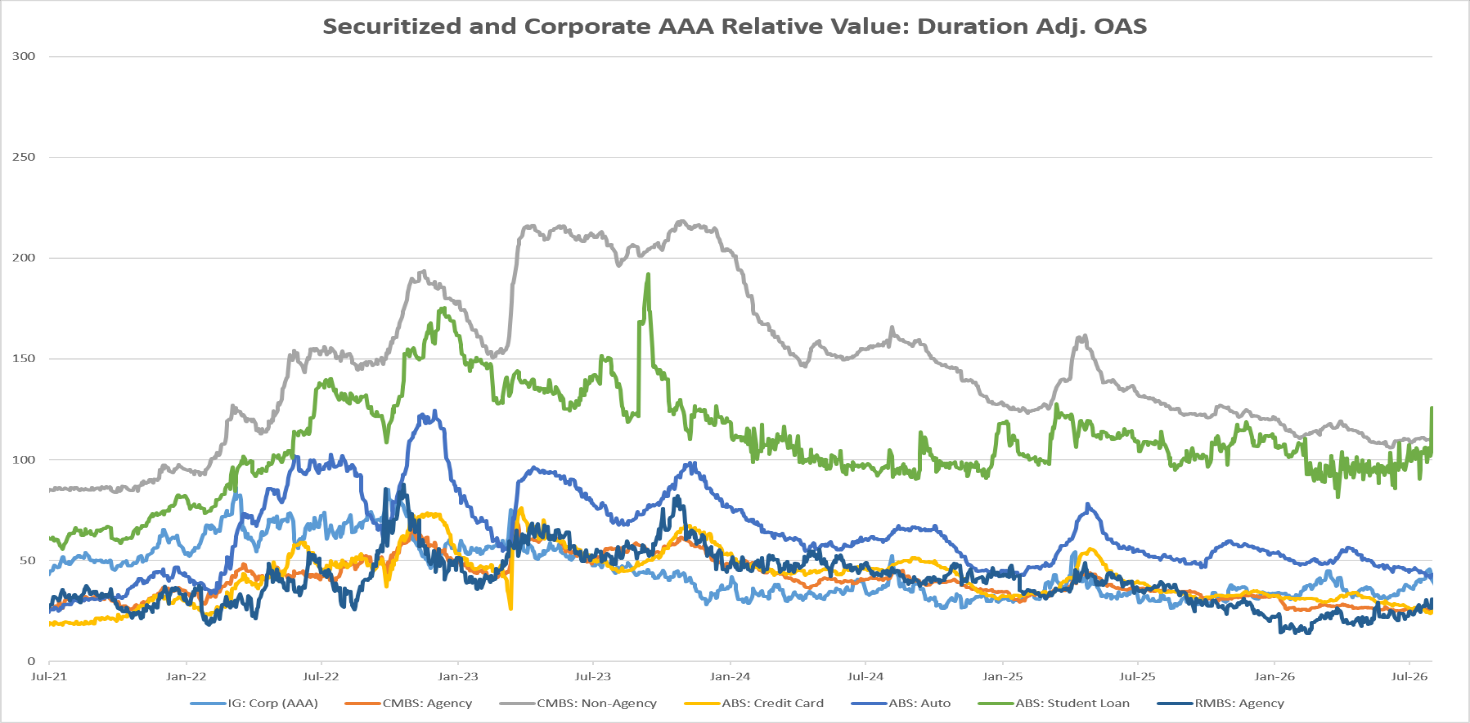

Diagram S: Structured Credit Spreads

Source: Bloomberg

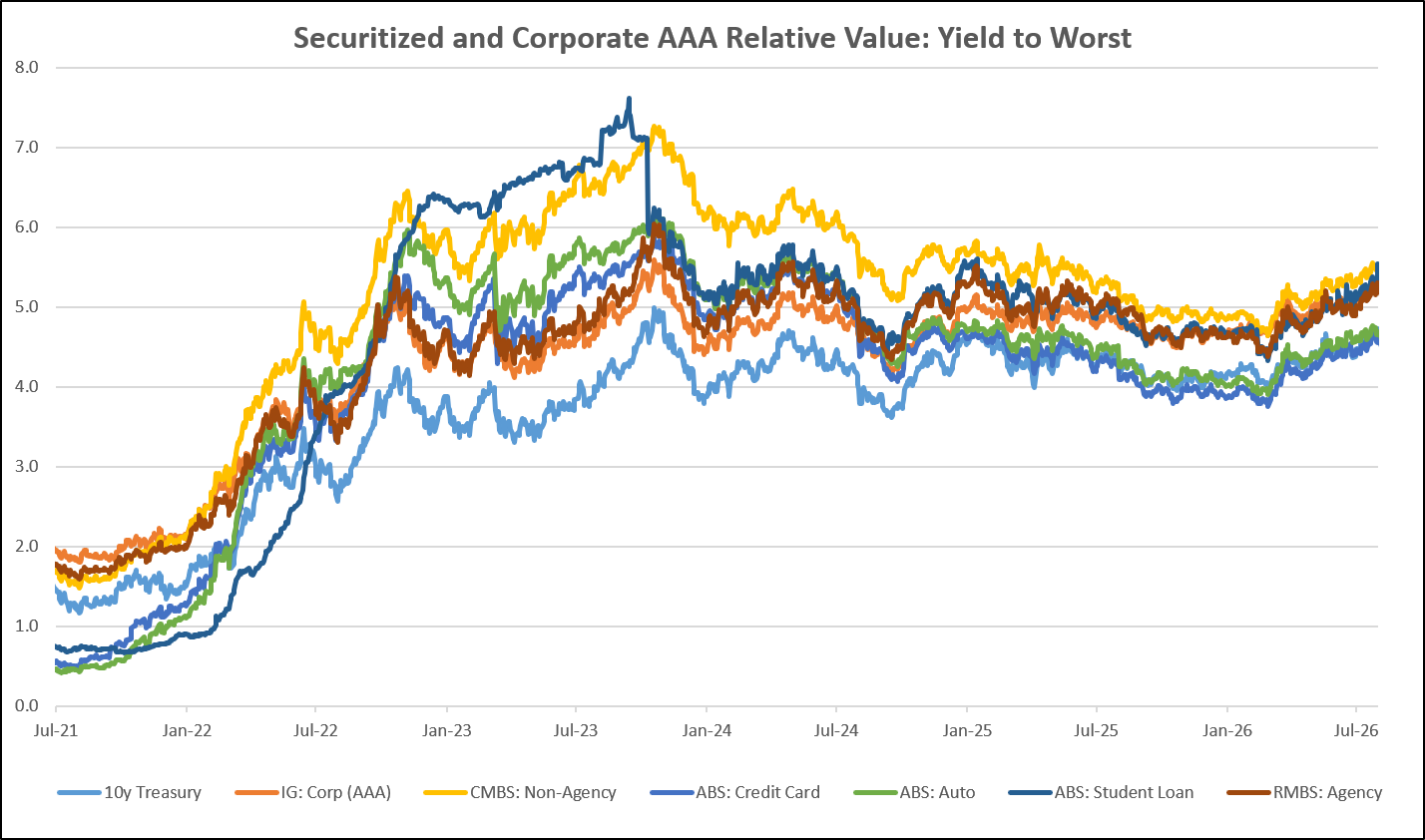

Diagram T: Structured Credit Yield

Source: Bloomberg

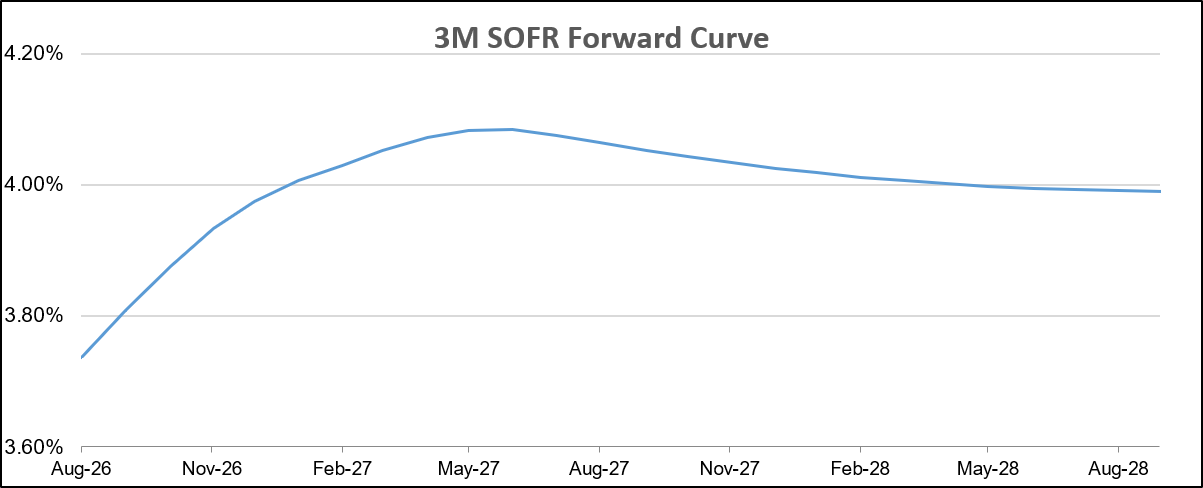

Diagram U: SOFR Curve

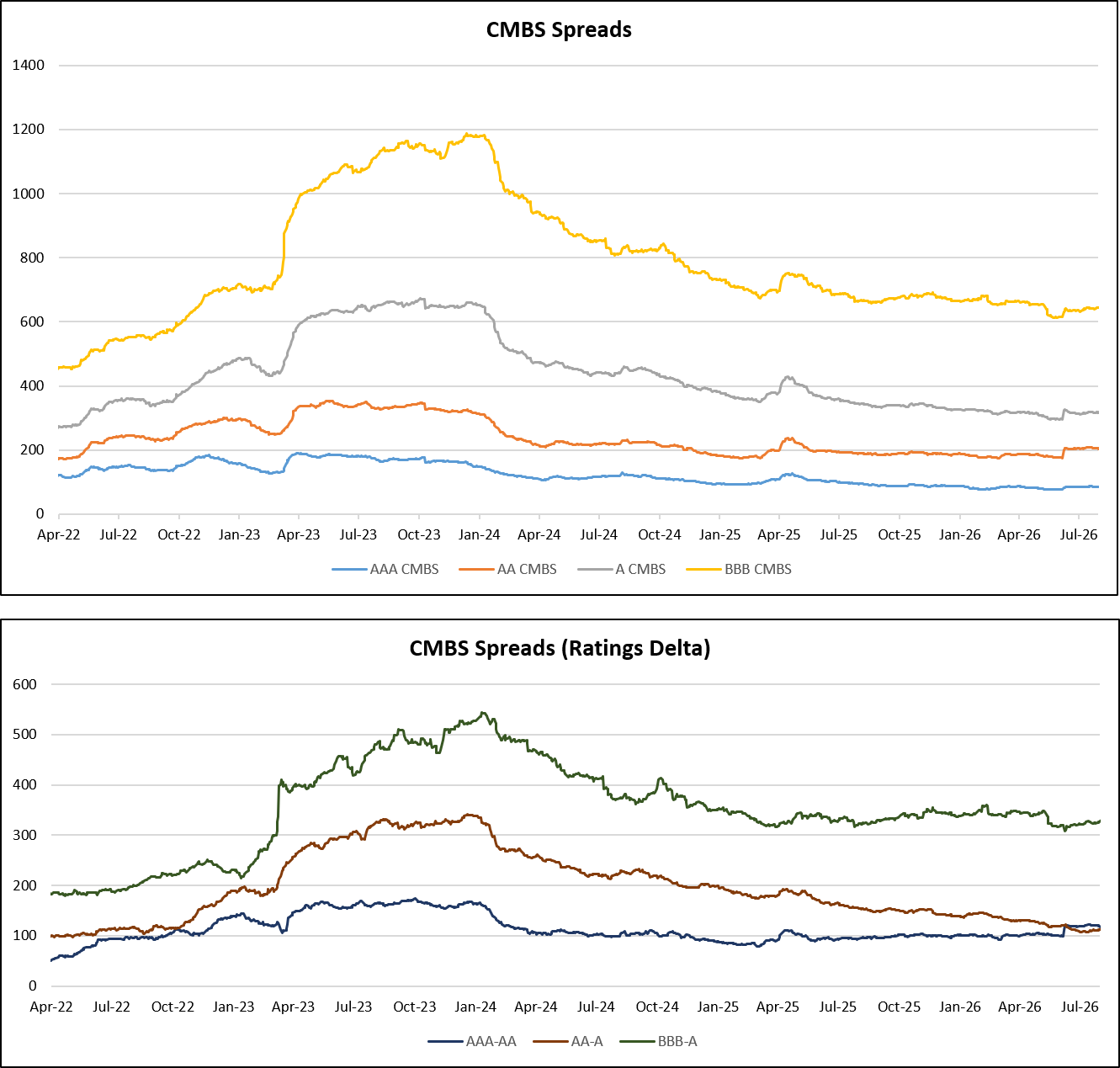

Diagram V: CMBS Spreads

Source: Bloomberg