.jpg)

SOCIAL SHARE

Mar 3, 2026

ZCG PE Insights: AI Capital Intensity and Inflation Dynamics

.jpg)

Projected AI-related capital expenditures are approaching $700 billion in 2026, with five-year commitments exceeding $5 trillion. This synchronized capital deployment is tightening supply in semiconductors, power infrastructure, and skilled labor markets, shifting cost curves before productivity gains diffuse.

Record data center construction growth, chip allocation shifts, and grid strain are concentrating demand in capacity-limited markets. In capital cycles where supply expansion lags demand, price becomes the adjustment mechanism.

Record bond issuance and rising leverage among infrastructure builders are heightening exposure to rate volatility. Modeling of anticipated adoption suggests inflationary pressure can persist during the investment phase, particularly when expectations accelerate capital formation.

The scale of current AI deployment more closely resembles prior industrial expansions than software cycles. Hyperscaler capital expenditures are projected to exceed $500 billion in 2026, with aggregate technology-sector investment approaching $700 billion(1). Five-year capital commitments are estimated near $5.2 trillion(2). The magnitude and simultaneity of this reallocation are unprecedented within a single technology vertical.

This concentration is occurring across advanced semiconductors, high-density data centers, networking equipment, and supporting energy infrastructure. As capital accelerates into fixed assets with long construction timelines, near-term supply elasticity remains limited. Macroeconomic modeling indicates that in anticipated adoption scenarios, inflation rises during the buildout phase as firms expand capital investment ahead of realized output gains(3). Expectations reinforce demand before incremental capacity normalizes pricing (4).

For investors, this dynamic alters underwriting assumptions. Input cost volatility, energy pricing, and hardware availability increasingly represent structural variables rather than cyclical noise. Businesses dependenton semiconductor supply, grid access, or large-scale computing resources are exposed to pricing pressure tied directly to hyperscale deployment cycles. Conversely, companies positioned within constrained infrastructure layers may benefit from durable demand visibility and pricing leverage.

The distinction between the investment cycle and theproductivity cycle is central. Productivity effects materialize gradually. Capital intensity is immediate.

Capital intensity alone does not sustain price pressure; constraint does. AI infrastructure depends on markets characterized by limited short-term capacity expansion. Advanced chip production, high-voltage transmission, specialized cooling systems, and skilled engineering labor represent bottlenecks with multi-year lead times.

AI-driven semiconductor demand has tightened supply and supported elevated component pricing, with spillover into adjacent hardware markets(5). Allocation decisions increasingly favor AI workloads over consumer and industrial end markets, elevating marginal costs beyond the technology sector.

Construction activity reinforces this pattern. Data center construction expanded approximately 32% year-over-year in 2025 while broader commercial construction activity remained subdued (5). Hyperscale facilities require specialized electrical systems, advanced cooling infrastructure, and skilled engineering labor. These labor markets are not infinitely scalable, and wage adjustment precedes workforce expansion when demand outpaces training pipelines.

Energy infrastructure presents an additional constraint. Large-scale facilities require sustained grid capacity, long-term power commitments, and significant cooling resources. Grid strain and allocation concerns have emerged in regions hosting concentrated deployment (4). Expanding transmission lines, generation capacity, and substation infrastructure requires multi-year capital programs and regulatory approvals. Forecasts indicate AI-related capital expenditures may continue tightening semiconductor availability and power capacity, with implications for regional energy pricing and industrial cost structures (1).

These dynamics illustrate a classical capital-cycle asymmetry. Demand associated with investment surges immediately; supply expansion follows a multi-year horizon. In systems characterized by constrained inputs serving multiple industries, incremental demand from one concentrated vertical alters pricing across the broader economy. The transmission is gradual but persistent. Until capacity materially expands, price becomes the clearing mechanism.

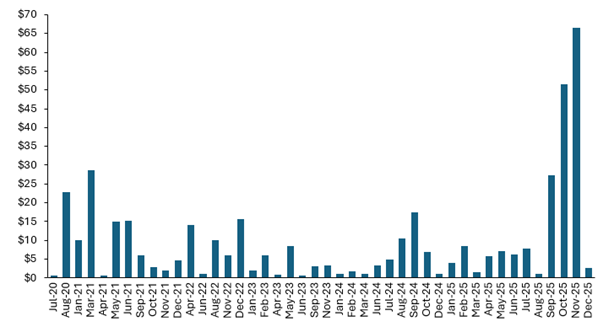

The financing structure of the AI expansion introduces additional sensitivity to interestrates and credit conditions. Investment-grade issuance by large technology firms reached $108.7 billion in the fourth quarter of 2025, positioning the sector as a dominant presence in corporate debt markets(6). As capital expenditures accelerate, free cash flow among major infrastructure builders has compressed and leverage has increased.

Historically, periods of rapid asset expansion have coincided with uneven equity outcomes, particularly when capacity growth ultimately exceeds demand. Infrastructure booms have frequently delivered transformative economic outcomes while generating mixed returns for capital providers. Builders operating within competitive ecosystems often captured narrower margins than expected once supply scaled.

Macroeconomic modeling suggests that in anticipated adoption scenarios, inflationary pressure may persist during the investment phase, increasing the probability that policy remains restrictive longer than forward curves imply(3). Higher real rates disproportionately affect asset-heavy operators with extended payback profiles and fixed financing commitments.

For sponsors, capital structure discipline becomes increasingly relevant. Elevated leverage in infrastructure-adjacent sectors heightens sensitivity to refinancing conditions and valuation multiples. Businesses positioned downstream of infrastructure expansion, users rather than builders, may ultimately capture more durable economics once capacity matures and input pricing stabilizes.

The interaction of capital intensity, balance sheet expansion, and constrained supply supports structurally higher nominal volatility during the buildout phase.

Sources

1 Macfarlanes,The Macroeconomic Backdrop to Private Capital Markets, February 2026

2 Morningstar,Why the AI Spending Spree Could Spell Trouble for Investors, 2025

3 Bank forInternational Settlements, The Impact of Artificial Intelligence on Outputand Inflation, Working Paper No. 1179

4 LondonSchool of Economics Business Review, AI Is Changing Inflation Dynamics andChallenging Central Banks, October 2025

5 TheWashington Post, The AI Boom Is So Huge It’s Causing Shortages EverywhereElse, 2025

6 TheWashington Post, Big Tech Is Taking on More Debt Than Ever Before to FundIts AI Aspirations, 2025

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 400 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.