.png)

SOCIAL SHARE

Apr 16, 2026

ZCGC Insights: Working Capital Is Physical — How Real Estate and Supply Chains Are Rewiring Liquidity

%20(2).jpg)

The operating environment has shifted. Balance-sheet discipline is now table stakes. What separates leading operators is execution, specifically how effectively they are using real estate and supply chain decisions to move capital through the system faster.Working capital is no longer a metric managed by finance. It is an outcome determined by where inventory sits, how space is deployed, and how procurement is timed. Organizations that treat these as operational details rather than capital decisions are leaving liquidity on the table. Across recent ZCGC engagements, the pattern is consistent: the most meaningful working capital improvements have come from changes to physical network design.

Recent engagements have surfaced specific areas where physical operations are absorbing capital that financial policy cannot recover. Dwell time has increased across multi-node networks. Inventory is sitting longer in lower-through put locations, tying up cash in positions that are neither serving demand nor moving toward conversion. Lease structures are misaligned with current inventory requirements. Footprints built for higher volume or different demand geography are carrying fixed obligations that no longer reflect operating reality. Vendor payment terms are out of sync with inventory cycles. Commitments locked in during higher-demand periods are creating cash flow mismatches that compound when inventory is being repositioned at the same time. Rising tariffs and input costs are increasing the capital intensity of inventory. As carrying costs rise, inventory turns become more critical, making stock management an increasingly important driver of cash flow. Each of these is a working capital problem with a physical solution.

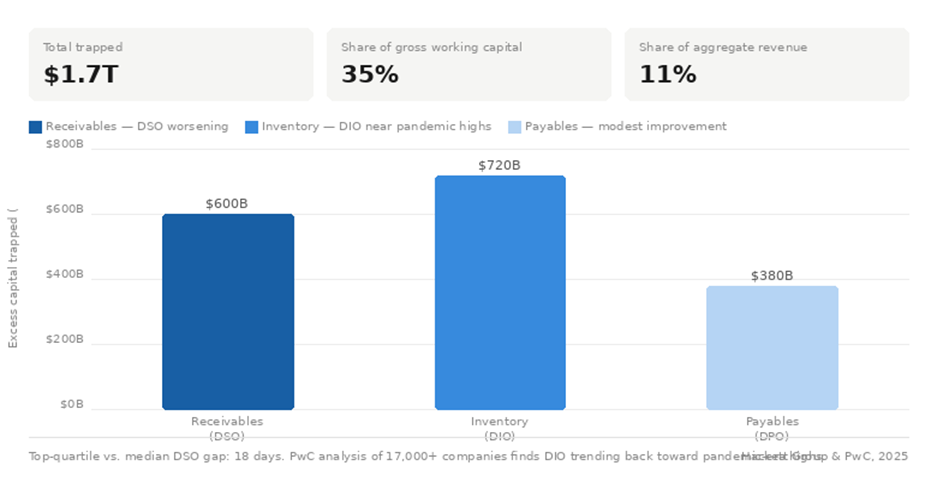

PwC's Working Capital Study 25/26, drawing on analysis of over 17,000 companies globally, found that days inventory outstanding is trending back toward pandemic-era highs, with financial levers largely exhausted as a tool for recovery. The Hackett Group's 2025 U.S. Working Capital Survey puts the consequence in concrete terms: $1.7 trillion remains trapped in excess working capital across the largest U.S. public companies, with inventory and receivables both worsening despite modest gains elsewhere. The remaining opportunity is operational.

The following reflects what is actually working across engagements, specific disciplines, not frameworks.

The most direct working capital improvement comes from getting inventory closer to where it converts. Organizations managing distribution across multiple nodes have found that stock concentrated in lower-throughput locations inflates dwell time and delays cash recovery, even when total inventory levels appear reasonable. The intervention is network rebalancing: consolidating volume into facilities with higher fulfillment velocity, reducing the number of nodes carrying safety stock, and redesigning routing to reflect actual demand geography rather than legacy footprint.In practice, this has reduced dwell time materially and improved inventory turnover without requiring changes to SKU rationalization or service commitments. The capital release is a direct function of where inventory sits, not how much of it there is.

Facilities with declining utilization carry a cost that compounds quietly. Fixed lease obligations, allocated overhead, and capital tied to space that is no longer earning its position in the network accumulate without triggering the same visibility as a balance sheet line item. The more effective operators are not waiting for lease expirations. They are identifying underutilized facilities early, assessing sublease potential and restructuring optionality while those levers are still available, and sequencing exits to align with network consolidation. In several cases this has involved consolidating two facilities into one higher-utilization node, reducing both fixed cost exposure and the working capital drag of split inventory positions. Underutilized space is not a real estate problem. It is a capital efficiency problem that happens to have a real estate solution.

Network proximity to demand centers directly affects how much buffer inventory an organization needs to carry. Facilities positioned further from demand require larger safety stock to maintain service levels, capital that sits idle most of the time and converts slowly when needed. Operators that have repositioned distribution nodes closer to primary demand geographies have reduced required buffer inventory by a measurable margin. The working capital impact is immediate: less inventory needed to achieve the same service outcome means faster conversion and lower average capital deployment. When the footprint change also reduces lease cost, the structural benefit compounds over the duration of the new commitment.

Procurement terms set the rhythm of cash outflow. When those terms are misaligned with inventory conversion cycles, particularly in categories where volume commitments were locked in during a different demand environment, the result is predictable cash drag that is difficult to offset through operations alone. The discipline here is renegotiation with visibility: adjusting payment windows and order cadence using current throughput and conversion data rather than terms that made sense under prior volume assumptions. In categories with meaningful spend, extending payment terms aligned with actual inventory turn produces a working capital improvement that is both immediate and recurring. This is not cost reduction. It is timing alignment. The same goods, the same vendors, the same prices, structured to move capital more efficiently through the cycle.

Real estate and supply chain decisions have always had financial consequences. What has changed is the degree to which those consequences are now the primary determinant of working capital performance.

ZCGC works alongside management teams to identify where capital is being absorbed by physical network inefficiencies and to design and execute the changes required to release it. The work spans distribution network design, real estate rationalization, lease restructuring, and procurement realignment, executed as an integrated program rather than independent workstreams.

The organizations that are winning on working capital are not doing anything exotic. They are managing their physical assets with the same rigor they apply to their financial ones.

The ability to generate liquidity from within the operating model rather than accessing it externally will remain a meaningful differentiator as conditions stay dynamic. The firms best positioned to act on this are those that have already aligned their physical network decisions with their capital objectives. For those that have not, the opportunity is tangible and the path is operational.

The constraint is no longer access to capital. It is how effectively capital moves through the system.

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 400 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.

ZCG Consulting (“ZCGC”) is the business consulting platform of ZCG and is a results‐oriented management consulting firm for middle market businesses. A reliable resource for private equity firms and their portfolio companies, our professionals offer deep functional expertise and customizable hands-on solutions to accelerate growth.

.png)